(Image credit: Getty Images)

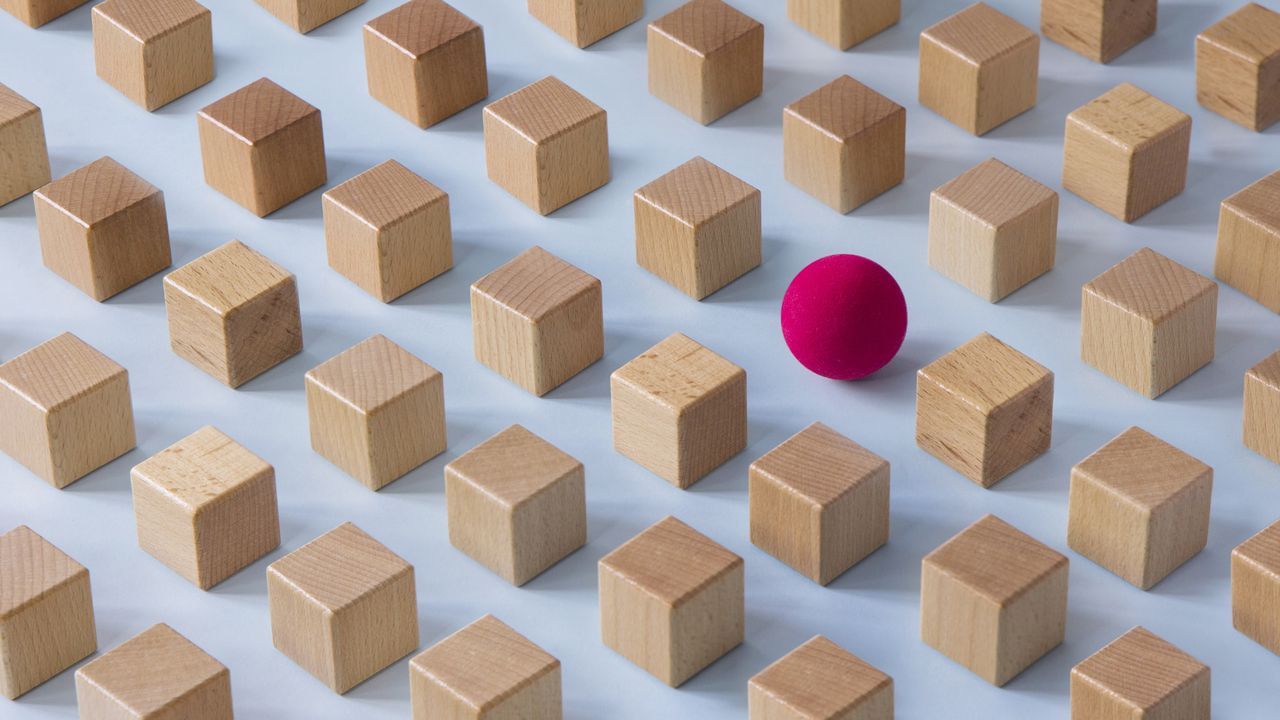

Some may remember the magnifying eyes of our youth while combing through tight quarters to find the candy-cane-striped, beanie-domed Waldo. There were a lot of masquerading Waldos, perhaps with the wire-framed glasses pushed to the side.

To our adult eyes, it’s kind of like finding that needle in a haystack. That one-in-a-million feeling isn’t as fond now; adulting pulls all of us in many different directions with many different decisions to make every day.

Some are simple — chicken or fish? — some are far more consequential, such as when to engage with a financial adviser and which one to choose.

From just $107.88 $24.99 for Kiplinger Personal Finance

Become a smarter, better informed investor. Subscribe from just $107.88 $24.99, plus get up to 4 Special Issues

CLICK FOR FREE ISSUE

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more – straight to your e-mail.

Profit and prosper with the best of expert advice – straight to your e-mail.

Historically, word of mouth has been a popular and convenient option. Someone you trust vouches for an adviser, so that trust seems applicable to your situation. It makes sense with the mistaken belief that all advisers pretty much have equal expertise.

Yet, your mom’s financial situation, goals and needs are far different from yours. Your 30-year-old, unmarried neighbor probably doesn’t need the same attention to complexity as your family, with an owned LLC, an ailing in-law and two kids approaching grade school.

The complex details matter

Every situation has some similarities. Common, and generally good, investment advice for a 40-year-old is to max out the company plan and traditional or Roth IRA, contribute to a brokerage account and let the compounding of time do its thing.

Yet, it’s in the complex details where having a financial adviser pays for itself many times over.

Navigating you through the impacts of small-business taxes, life insurance needs, the use of HSAs and 529s, the time horizon of retirement and — over time — all of the decisions that come with that life stage is invaluable.

That’s where referrals can be hit-or-miss. Even with a referral, more people are leaning into big brands they know or using an online search tool to find an adviser based on geography, need, behavioral connection or a combination of the three.

Yet, most search tools are limited, spinning up lists of advisers by ZIP code even though COVID-19 completely shattered the proximity paradigm.

Or the tools roll out a list of Waldo lookalikes. They have bios that sound the same, and they all say they offer the same 10 to 12 services under a “comprehensive” planning model.

How do you tell advisers apart?

Most of them aren’t who you need, but there’s no way to tell them apart. That’s the challenge consumers continue to draw out in countless research studies.

They are searching for an adviser to help with very specific goals (i.e., a specialist) amid a sea of generalists masquerading as far more.

Imagine that happening in the medical or law profession. A family doctor saying they perform heart surgery? A real estate attorney navigating you through a divorce?

If clients live specialized lives (unique and complex), they require a true team of generalists and specialists to empower their success. And they need an easy way to find them.

Why to use a financial adviser

The American College of Financial Services partnered with Endeavor Business Intelligence as part of a research project to best understand the drivers of adviser selection.

Consumers who currently use financial advisers identify a combination of convenience, trust and professional expertise.

Others value the adviser’s specialized knowledge, especially in areas like retirement planning; however, they acknowledge that they kind of “lucked out,” as there was no easy way to distinguish between advisers or no one great question to raise a red flag in an initial meeting.

Unpacking those three differentiators, respondents to a 500-person survey indicate little time to learn how to navigate finances on their own. They highlight trust earned over time as invaluable. And they stress that true experts are “worth the cost,” as they help grow and protect assets and offer equally important peace of mind.

A very interesting nugget came out of follow-up questions. Consumers often conflate experience with expertise. Why? First, it’s easily quantifiable when selecting between a 30-year veteran and a 30-year-old just out on their own.

Experience tends to forge trust in so many of our life decisions as well. Yet, we also found that experience tends to be a proxy for expertise since gauging expertise is so much harder in the advisory search.

That’s the rub. Haven’t consumers read the “Past performance is not indicative of future results” disclosure? Length of service isn’t always correlated to success.

Even if it were, success looks different for those with an adviser who builds and monitors low-cost, accumulation-focused portfolios vs those whose adviser navigates tax and timing pitfalls in retirement.

It’s like saying a pitmaster has the same skills as a sushi chef.

Actionable steps to identify a true specialist

If you wouldn’t trust a pitmaster to prepare blowfish, you shouldn’t assume every adviser can handle the nuanced needs of your financial life. To go beyond the basics of checking credentials, consider these deeper, practical steps:

Ask for real examples of cases like yours. Not hypotheticals — actual anonymized client scenarios. Specialists should be able to articulate how they’ve handled situations nearly identical to yours, whether that’s stock-option exercise timing, multigenerational planning or Medicare’s IRMAA surcharges.

Request their “circle of specialists.” Strong advisers know what they don’t know. Ask who they collaborate with — estate attorneys, CPAs, business valuation experts, insurance specialists — and how often they integrate those experts into client work. True specialists rarely operate solo.

Have them map your complexity. A skilled adviser should be able to sketch out (even on a notepad) the major areas of financial impact in your life and the decision points ahead.

Press for their process, not their pitch. Ask: “Walk me through your planning process from first meeting to recommendation.” Generalists talk about products. Specialists talk about process, diagnostics and measurable outcomes.

Test their depth on one issue you care about. Pick a topic — 529 strategies, RMD planning, business-owner succession, insurance contract structures and ask two follow-ups. Shallow answers quickly reveal shallow expertise.

These steps make it easier to separate the real Waldo from the lookalikes.

Either way, the future is for specialists. Consumers already want and need them. Over time, the decision tree won’t look like a mess of blurry lines. Finding the real Waldo will be clear, and it will come with a sound financial future.

Related Content

This article was written by and presents the views of our contributing adviser, not the Kiplinger editorial staff. You can check adviser records with the SEC or with FINRA.